Lumb Accountancy Services

Lumb Accountancy Services

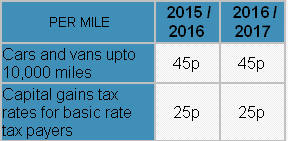

PER MILE

|

2012 / 2013

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

Cars and vans upto 10,000 miles

|

45p

|

45p

|

45p

|

45p

|

45p

|

Capital gains tax rates for basic rate tax payers

|

25p

|

25p

|

25p

|

25p

|

25p

|

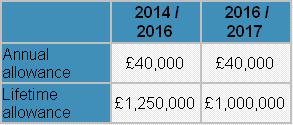

2011 / 2012

|

2012 / 2013

|

2013 / 2014

|

2014 / 2016

|

2016 / 2017

|

|

Annual allowance

|

£50,000

|

£50,000

|

£40,000

|

£40,000

|

£40,000

|

Lifetime allowance

|

£1,500,000

|

£1,500,000

|

£1,250,000

|

£1,250,000

|

£1,000,000

|

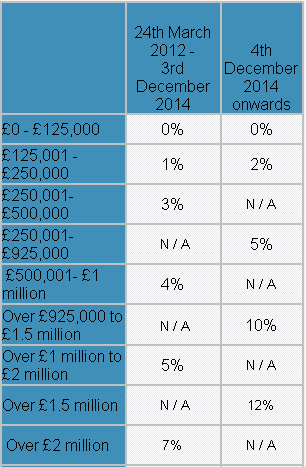

24th March 2012 -

3rd December 2014

|

4th December

2014 onwards

|

|

£0 - £125,000

|

0%

|

0%

|

£125,001 -£250,000

|

1%

|

2%

|

£250,001-£500,000

|

3%

|

N / A

|

£250,001- £925,000

|

N / A

|

5%

|

£500,001- £1 million

|

4%

|

N / A

|

Over £925,000 to £1.5 million

|

N / A

|

10%

|

Over £1 million to £2 million

|

5%

|

N / A

|

Over £1.5 million

|

N / A

|

12%

|

Over £2 million

|

7%

|

N / A

|

PER MILE

|

2012 / 2013

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

Cars and vans upto 10,000 miles

|

45p

|

45p

|

45p

|

45p

|

45p

|

Capital gains tax rates for basic

rate tax payers

|

25p

|

25p

|

25p

|

25p

|

25p

|

2011 / 2012

|

2012 / 2013

|

2013 / 2014

|

2014 / 2016

|

2016 / 2017

|

|

Annual allowance

|

£50,000

|

£50,000

|

£40,000

|

£40,000

|

£40,000

|

Lifetime allowance

|

£1,500,000

|

£1,500,000

|

£1,250,000

|

£1,250,000

|

£1,000,000

|

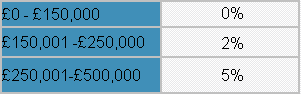

£0 - £150,000

|

0%

|

£150,001 -£250,000

|

2%

|

£250,001-£500,000

|

5%

|

£0 - £150,000

|

0%

|

£150,001 -£250,000

|

2%

|

£250,001-£500,000

|

5%

|