Lumb Accountancy Services

Lumb Accountancy Services

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

2017

/ 2018

|

|

Personal allowance (born after 05.04.48)

|

£9,440

|

£10,000

|

£10,600

|

£11,000

|

£11,500

|

Personal allowance (born 05.04.38 - 06.04.48)1

|

£10,500

|

£10,500

|

£10,600

|

£11,000

|

£11,500

|

Personal allowance (born before 06.04.38)2

|

£10,660

|

£10,660

|

£10,660

|

£11,000

|

£11,500

|

Income limit for personal allowance

|

£100,000

|

£100,000

|

£100,000

|

£100,000

|

£100,000

|

Income limit for age related allowances

|

£26,100

|

£27,000

|

£27,700

|

N/A

|

N/A

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

2017 / 2018

|

|

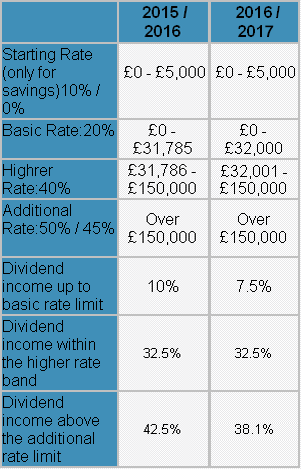

Starting Rate (only for savings)4 10% / 0%

|

£0 - £2,790

|

£0 - £2,880

|

£0 - £5,000

|

£0 - £5,000

|

£0 - £5,000

|

Basic Rate: 20%

|

£0 - £32,010

|

£0 - £31,865

|

£0 - £31,785

|

£0 - £32,000

|

£0 - £33,500

|

Higher Rate: 40%

|

£32,011 -

£150,000

|

£31,866 -

£150,000

|

£31,786 -

£150,000

|

£32,001 -

£150,000

|

£33,501 -

£150,000

|

Additional Rate: 45%

|

Over £150,000

|

Over £150,000

|

Over £150,000

|

Over £150,000

|

Over £150,000

|

Dividend income up to basic rate limit

|

10% (0%)3

|

10% (0%)3

|

10% (0%)3

|

7.5%

|

7.5%

|

Dividend income within the higher rate band

|

32.5% (25%)3

|

32.5% (25%)3

|

32.5% (25%)3

|

32.5%

|

32.5%

|

Dividend income above the additional rate limit

|

37.5% (30.56%)3

|

37.5% (30.56%)3

|

37.5% (30.56%)3

|

38.1%

|

38.1%

|

£ per week

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

2017 / 2018

|

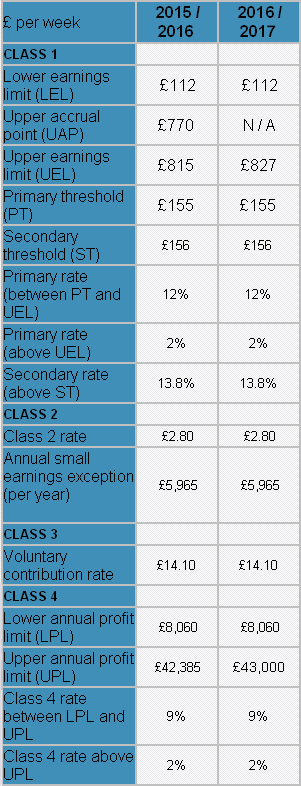

CLASS 1

|

|||||

Lower earnings limit (LEL)

|

£109

|

£111

|

£112

|

£112

|

£113

|

Upper accrual point (UAP)

|

£770

|

£770

|

£770

|

N / A

|

N / A

|

Upper earnings limit (UEL)

|

£797 | £805

|

£815

|

£827

|

£866

|

Primary threshold (PT)

|

£149 | £153

|

£155

|

£155

|

£157

|

Secondary threshold (ST)

|

£148

|

£153

|

£156

|

£156

|

£157

|

Primary rate (between PT and UEL)Primary rate (between PT and UEL)

|

12%

|

12%

|

12%

|

12%

|

12%%

|

Primary rate (above UEL)

|

2%

|

2%

|

2%

|

2%

|

2%%

|

Secondary rate (above ST)

|

13.8%

|

13.8%

|

13.8%

|

13.8%

|

13.8%%

|

CLASS 2

|

|||||

Class 2 rate

|

£2.70 |

£2.75

|

£2.80

|

£2.80

|

£2.85

|

Sll eaprofits

threshold amount r year)

|

£5,725 |

£5,885

|

£5,965

|

£5,965

|

£6,025

|

CLASS 3CLASS 3

|

|||||

Voluntary contribution rate

|

£13.55

|

£13.90

|

£14.10

|

£14.10

|

£14.25

|

CLASS 4

|

|||||

Lower annual profit limit (LPL)

|

£7,755

|

£7,956

|

£8,060

|

£8,060

|

£8,164

|

Upper annual profit limit (UPL)

|

£41,450

|

£41,865

|

£42,385

|

£43,000

|

£45,000

|

Class 4 rate between LPL and UPLClass 4 rate between LPL and UPL

|

9%

|

9%

|

9%

|

9%

|

9%%

|

Class 4 rate above UPL

|

2%

|

2%

|

2%

|

2%

|

2%

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

2017 / 2018

|

|

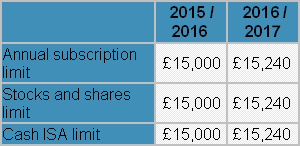

Annual subscription limit

|

£15,000

|

£15,000

|

£15,240

|

£15,240

|

£20,000

|

Stocks and shares limit

|

£11,520

|

£15,000

|

£15,240

|

£15,240

|

£20,000

|

Cash ISA limit

|

£5,760

|

£15,000

|

£15,240

|

£15,240

|

£20,000

|

2012 / 2013

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

|

Personal allowance (born after

05.04.48)

|

£8,105

|

£9,440

|

£10,000

|

£10,600

|

£11,000

|

Personal allowance (born

05.04.38 - 06.04.48)

|

£10,500

|

£10,500

|

£10,500

|

£10,600

|

£11,000

|

Personal allowance (born before

06.04.38)

|

£10,660

|

£10,660

|

£10,660

|

£10,660

|

£11,000

|

Income limit for personal

allowance

|

£100,000

|

£100,000

|

£100,000

|

£100,000

|

£100,000

|

Income limit for age related

allowances

|

£25,400

|

£26,100

|

£27,000

|

£27,700

|

N/A

|

2012 / 2013

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

|

Starting Rate (only for savings)

10% / 0%

|

£0 - £2,710

|

£0 - £2,790

|

£0 - £2,880

|

£0 - £5,000

|

£0 - £5,000

|

Basic Rate:

20%

|

£0 - £34,370

|

£0 - £32,010

|

£0 - £31,865

|

£0 - £31,785

|

£0 - £32,000

|

Highrer Rate:

40%

|

£34,371 -

£150,000

|

£32,011 -

£150,000

|

£31,866 -

£150,000

|

£31,786 -

£150,000

|

£32,001 -

£150,000

|

Additional Rate:

50% / 45%

|

Over

£150,000

|

Over

£150,000

|

Over

£150,000

|

Over

£150,000

|

Over

£150,000

|

Dividend income up to basic rate

limit

|

10% (0%)

|

10% (0%)

|

10% (0%)

|

10%

|

7.5%

|

Dividend income within the

higher rate band

|

32.5% (25%)

|

32.5% (25%)

|

32.5% (25%)

|

32.5%

|

32.5%

|

Dividend income above the

additional rate limit

|

38.1% (30.6%)

|

38.1% (30.6%)

|

38.1% (30.6%)

|

42.5%

|

38.1%

|

£ per week

|

2012 / 2013

|

2013 / 2014

|

2014 / 2015

|

2015 / 2016

|

2016 / 2017

|

CLASS 1

|

|||||

Lower earnings limit (LEL)

|

£107

|

£109

|

£111

|

£112

|

£112

|

Upper accrual point (UAP)

|

£770

|

£770

|

£770

|

£770

|

N / A

|

Upper earnings limit (UEL)

|

£817

|

£797

|

£805

|

£815

|

£827

|

Primary threshold (PT)

|

£146

|

£149

|

£153

|

£155

|

£155

|

Secondary threshold (ST)

|

£144

|

£148

|

£153

|

£156

|

£156

|

Primary rate (between PT and

UEL)

|

12%

|

12%

|

12%

|

12%

|

12%

|

Primary rate (above UEL)

|

2%

|

2%

|

2%

|

2%

|

2%

|

Secondary rate (above ST)

|

13.8%

|

13.8%

|

13.8%

|

13.8%

|

13.8%

|

CLASS 2

|

|||||

Class 2 rate

|

£2.65

|

£2.70

|

£2.75

|

£2.80

|

£2.80

|

Annual small earnings

exception (per year)

|

£5,595

|

£5,725

|

£5,885

|

£5,965

|

£5,965

|

CLASS 3

|

|||||

Voluntary contribution rate

|

£13.25

|

£13.55

|

£13.90

|

£14.10

|

£14.10

|

CLASS 4

|

|||||

Lower annual profit limit (LPL)

|

£7,605

|

£7,755

|

£7,956

|

£8,060

|

£8,060

|

Upper annual profit limit (UPL)

|

£42,475

|

£41,450

|

£41,865

|

£42,385

|

£43,300

|

Class 4 rate between LPL and

UPL

|

9%

|

9%

|

9%

|

9%

|

9%

|

Class 4 rate above UPL

|

2%

|

2%

|

2%

|

2%

|

2%

|